2023-0964351C6 Question 6 – Application of the Canada-US Treaty

Please note that the following document, although believed to be correct at the time of issue, may not represent the current position of the CRA. Prenez note que ce document, bien qu'exact au moment émis, peut ne pas représenter la position actuelle de l'ARC.

Principal Issues:

Does the Treaty apply to exempt the interest from the Canadian withholding tax in the described structures involving fiscally transparent entities?

Position:

Basic Structure – No; First modified structure - Yes; Second modified structure – Yes.

Reasons:

Application of the Treaty and prior positions.

Author:

Chan, Michael

Section:

Paragraph 212(13)(f), 212(13.2)(b), Article IV(6), Article XI, Article XXIX-A

2023 IFA Annual Conference

CRA Roundtable

Question 6: Application of the Canada-U.S. Income Tax Convention to Structures with Multiple Tiers of Fiscally Transparent Entities

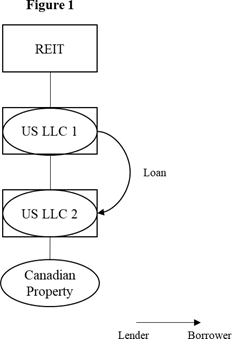

A U.S. resident corporation that has elected to be classified as a “real estate investment trust” (“REIT”) under the applicable provisions of the U.S. Internal Revenue Code (the “Code”) is a regarded entity for U.S. income tax purposes. REIT owns US LLC 1, a disregarded entity for U.S. income tax purposes. US LLC 1 owns US LLC 2, also a disregarded entity for U.S. income tax purposes and a section 216 taxpayer for Canadian income tax purposes. Neither US LLC 1 nor US LLC 2 is a resident of Canada for the purposes of the Canada-U.S. Income Tax Convention (the “Treaty”).

US LLC 1 makes an interest bearing loan to US LLC 2. The loan is incurred in connection with US LLC 2’s real estate operations in Canada, which constitute its permanent establishment in Canada, and the interest on the loan is borne by the permanent establishment. A pictorial illustration is provided in figure 1.

{kind=link}

Assume that the interest income is subject to Canadian Part XIII withholding tax (either as a result of the application of paragraph 212(13)(f) or proposed paragraph 212(13.2)(b) of the Act).

In technical interpretation 2012-0434311E5, in the context of a disregarded Canadian unlimited liability company making payments to a disregarded U.S. limited liability company (“LLC”), the CRA had stated that Article IV(6) of the Treaty would not apply to treat a particular amount of Canadian-source income, profit or gain as being derived by the U.S. member(s) of a fiscally transparent entity where that amount is “disregarded” under the taxation laws of the U.S. The same conclusion applies in respect of the basic structure described herein.

Will the Treaty apply to exempt the interest from the Canadian withholding tax if the basic structure is modified as described in the scenarios below?

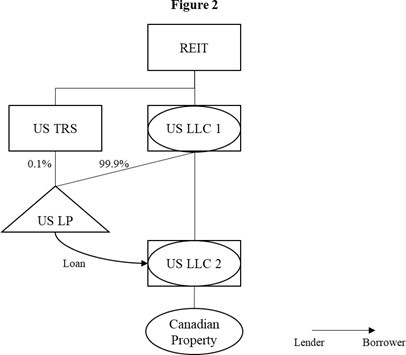

The basic structure is modified to create a regarded interest recipient for U.S. income tax purposes (“first modified structure”) (see figure 2):

{kind=link}

* REIT incorporates a new corporation (“US TRS”) with a nominal share capital. REIT and US TRS jointly elect to treat US TRS as a taxable REIT subsidiary under the Code. US TRS is a taxable corporation (and is regarded) for U.S. income tax purposes.

* Both REIT and US TRS are U.S. residents for the purposes of the Treaty and “qualifying persons” within the meaning of Article XXIX-A of the Treaty.

* Neither REIT nor US TRS carries on or has carried on business in Canada through a permanent establishment.

* US LLC 1 and US TRS form US LP, a limited partnership formed under the laws of the U.S. US TRS holds 0.1% general partner interest in US LP, while US LLC 1 holds 99.9% limited partner interest.

* US LP is considered a flow-through entity for U.S. income tax purposes, but is not disregarded.

* US LP, rather than US LLC 1, makes an interest bearing loan to US LLC 2.

* For U.S. income tax purposes, interest paid by US LLC 2 to US LP is viewed as interest paid by REIT to US LP and it is not disregarded.

* On an annual basis REIT and US TRS are allocated interest income received by US LP in proportion to their partnership interests and include it in computing their taxable income for U.S. income tax purposes as interest income.

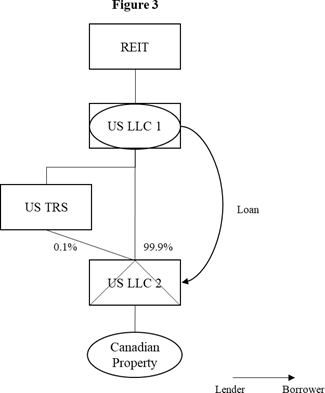

Alternatively, the basic structure is instead modified to make the payor of the interest regarded for the U.S. income tax purposes (“second modified structure”) (see figure 3):

{kind=link}

* US LLC 1 incorporates a new corporation (“US TRS”) with a nominal share capital. US LLC 1 and US TRS jointly elect to treat US TRS as a taxable REIT subsidiary under the Code. US TRS is a taxable corporation (and is regarded) for U.S. income tax purposes.

* Both REIT and US TRS are U.S. residents for the purposes of the Treaty and “qualifying persons” within the meaning of Article XXIX-A of the Treaty.

* Neither REIT nor US TRS carries on or has carried on business in Canada through a permanent establishment.

* US TRS subscribes for 0.1% membership interest in US LLC 2, while US LLC 1 holds 99.99% of the membership interest.

* US LLC 2 is treated as a partnership for U.S. income tax purposes, which is a flow-through entity, but is not disregarded for U.S. income tax purposes.

* US LLC 1 makes an interest bearing loan to US LLC 2.

* For U.S. income tax purposes, interest paid by US LLC 2 to US LLC 1 is viewed as interest paid by US LLC 2 to REIT and it is not disregarded.

* REIT includes the amount of interest received as interest income from US LLC 2 through US LLC 1 in computing its taxable income for U.S. income tax purposes.

CRA Response

Pursuant to Article XI(1) of the Treaty, interest arising in Canada and beneficially owned by a resident of the U.S. may be taxed only in the U.S. In each of the three scenarios above, interest paid by US LLC 2 shall be deemed to arise in Canada pursuant to Article XI(4) of the Treaty on the basis that US LLC 2 has a permanent establishment in Canada in connection with which the indebtedness was incurred, and such interest is borne by such permanent establishment. Thus, the only question under consideration is whether the interest is beneficially owned by a resident of the U.S.

Pursuant to Article IV(6), an amount of income, profit or gain shall be considered to be derived by a person resident in the U.S. if, under U.S. income tax laws, the person is considered to derive the amount through a fiscally transparent entity that is not a resident of Canada, and by reason of the entity being fiscally transparent under U.S. laws, the U.S. income tax treatment of the amount is the same as the U.S. income tax treatment would be had the person derived the amount directly (the “same tax treatment” condition). In performing a comparative analysis to determine if an item of income receives the same tax treatment as if it had been derived directly by the person resident in the U.S., the timing of income recognition as well as the character and quantum of the income amount for tax purposes would be relevant factors. (footnote 1)

CRA's longstanding position for an LLC that is fiscally disregarded in the U.S., is that, without the application of Article IV(6) of the Treaty, the benefits provided under Article XI of the Treaty are not available in respect of the interest paid to the LLC. That conclusion is based on the fact that from a Canadian perspective, the U.S. LLC is not considered to be a resident of the U.S. for purposes of the Treaty.

As pointed out in the question, the CRA had concluded in technical interpretation 2012-0434311E5 that Article IV(6) of the Treaty would not apply to treat a particular amount of Canadian-source income, profit or gain that is “disregarded” under the taxation laws of the U.S. as being derived by the U.S. member(s) of a fiscally transparent entity and the CRA’s conclusion would be the same in respect of the base structure depicted in Figure 1 above.

First Modified Structure:

In applying the Treaty to amounts paid to or derived by a partnership, it is CRA’s long standing practice to look through the partnership such that the partners are viewed as the taxpayers who may invoke the benefits of the Treaty, subject, among other things, to the rules provided under Article XXIX-A of the Treaty. Accordingly, where a member of a partnership is a U.S. resident, the CRA considers the member's share of the income of the partnership to be derived by that member for purposes of applying the Treaty.

For purposes of applying Article XI of the Treaty, interest payments made by US LLC 2 to US LP will be considered to be derived by the members of US LP in proportion to their share of the income of US LP. Based on the facts, US TRS would be entitled to the benefits under the Treaty and would be exempt pursuant to Article XI(1) of the Treaty from withholding tax under Part XIII of the Act on the interest income derived by US TRS.

As for the remaining amount of the interest income of US LP that is allocated to US LLC 1, the latter will only be exempt pursuant to Article XI(1) of the Treaty from the Canadian withholding tax if the amount is considered to be derived by REIT pursuant to Article IV(6) of the Treaty. According to the question, for U.S. income tax purposes, US LLC 1 is fiscally transparent and the amount of the interest income of US LP that is allocated to US LLC 1 is considered to be derived by REIT and that interest income is included in computing REIT’s income for the taxation year of REIT in which the payment of interest is received by US LP. Thus, the U.S. income tax treatment of the interest received by US LP and indirectly allocated to REIT is the same as the U.S. income tax treatment would be had REIT derived the amount directly from US LP. Therefore, the same tax treatment condition would be met in this case and Article IV(6) would apply to grant the benefits under the Treaty to REIT in respect of its proportionate share of the interest income, which would also be exempt from withholding tax under Part XIII of the Act pursuant to Article XI(1) of the Treaty.

Second Modified Structure:

Based on the assumptions provided, the interest income on the loan owing by US LLC 2 to US LLC 1 would meet the same tax treatment condition for the purposes of applying Article IV(6) of the Treaty since the U.S. income tax treatment of interest income to REIT is the same as the U.S. income tax treatment would be had REIT received the interest income directly from US LLC 2. Therefore, the conditions of application of Article IV(6) of the Treaty would be met to grant the benefits under the Treaty to REIT in respect of the interest income that is derived by REIT for U.S. income tax purposes and for the purposes of the Treaty. Accordingly, the interest income is exempt from withholding tax under Part XIII of the Act pursuant to Article XI(1) of the Treaty.

Other considerations:

It should be noted that contemplated legislative proposals that would implement the recommendations in the Action 2 Report of the Organization for Economic Cooperation and Development /G20 Base Erosion and Profit Shifting project, on “Neutralizing the Effects of Hybrid Mismatch Arrangements” may have an impact on the structures described in this response.

Michael Chan

2023-096435

May 17, 2023

FOOTNOTES

Note to reader: Because of our system requirements, the footnotes contained in the original document are shown below instead:

1 Technical interpretation 2009-0318491I7.

All rights reserved. Permission is granted to electronically copy and to print in hard copy for internal use only. No part of this information may be reproduced, modified, transmitted or redistributed in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, or stored in a retrieval system for any purpose other than noted above (including sales), without the prior written permission of Canada Revenue Agency, Ottawa, Ontario K1A 0L5.

© His Majesty the King in Right of Canada, 2023

Tous droits réservés. Il est permis de copier sous forme électronique ou d'imprimer pour un usage interne seulement. Toutefois, il est interdit de reproduire, de modifier, de transmettre ou de redistribuer de l'information, sous quelque forme ou par quelque moyen que ce soit, de façon électronique, mécanique, photocopies ou autre, ou par stockage dans des systèmes d'extraction ou pour tout usage autre que ceux susmentionnés (incluant pour fin commerciale), sans l'autorisation écrite préalable de l'Agence du revenu du Canada, Ottawa, Ontario K1A 0L5.

© Sa Majesté le Roi du Chef du Canada, 2023

Video Tax News is a proud commercial publisher of Canada Revenue Agency's Technical Interpretations. To support you, our valued clients and your network of entrepreneurial, small businesses, we choose to offer this valuable resource to Canadian tax professionals free of charge.

For additional commentary on Technical Interpretations, court cases, government releases, and conference materials in a single practical document specifically geared toward owner-managed businesses see the Video Tax News Monthly Tax Update newsletter. This effective summary and flagging tool is the most efficient way to ensure that you, your firm, and your clients are fully supported and armed for whatever challenges are thrown your way. Packages start at $400/year.